CLICK THE PIC TO WATCH DAVE WRIGHT AND THE PURPLE PIPE WITH THE HD EFFECT!

CLICK THE PIC TO WATCH DAVE WRIGHT AND THE PURPLE PIPE WITH THE HD EFFECT!

To the extent tiered water rates are imposed in a manner that deviates from “cost of service” requirements, those rates are in violation of Proposition 218 -Howard Jarvis Taxpayer Association

UPDATE:04/09/2012: BARBER THE BLOGGER

It appears that for the most part the public may be a bit ‘confused’, a slight infusion of assurance in that it is not always ‘necessary’ to respond to the public’s questions. It looks as if there is still much to ‘ferret out’ within the city manager Scott Barber’s new position as city blogger…

He said he doesn’t always feel it’s necessary or appropriate to respond to the public’s questions and criticisms, but in this case, “I do believe there’s some confusion about what happened and what’s allowable and what’s not.”

A Moreno Valley community activist has filed a complaint with the California attorney general’s office seeking an investigation into the relationship between the City Council and developer Iddo Benzeevi.

In the City of Redlands, City Employee Bob Platt airs complaints against City Council.. Will he be blackballed? The Press Enterprise is reporting on outside city events more than the expolosion that has been happening in the City of Riverside.. what ties does the PE have with the City of Riverside?

Los Angeles facing a $222,000 million budget shortfall! City of Los Angeles also received the Achievement for Excellence in Financial Reporting by the Government Finance Officers Association for their 2009 CAFR.

Hercules, CA on the brink of bankruptcy, second to Stockton, CA? Hercules became the third city to undergo an audit by State Controller John Chiang ( the other two were Bell and Montebello). All three city’s have recieved the achievement for excellence in financial reporting, including recently, the City of Riverside. Part of Hercules economic hangover is a pair of four-story, half-finished, plastic-wrapped apartment buildings in Hercules. The city sank $38 million into those buildings, a 144,000-square-foot redevelopment project gone awry. Last week, the City Council sold the buildings for $425,000.

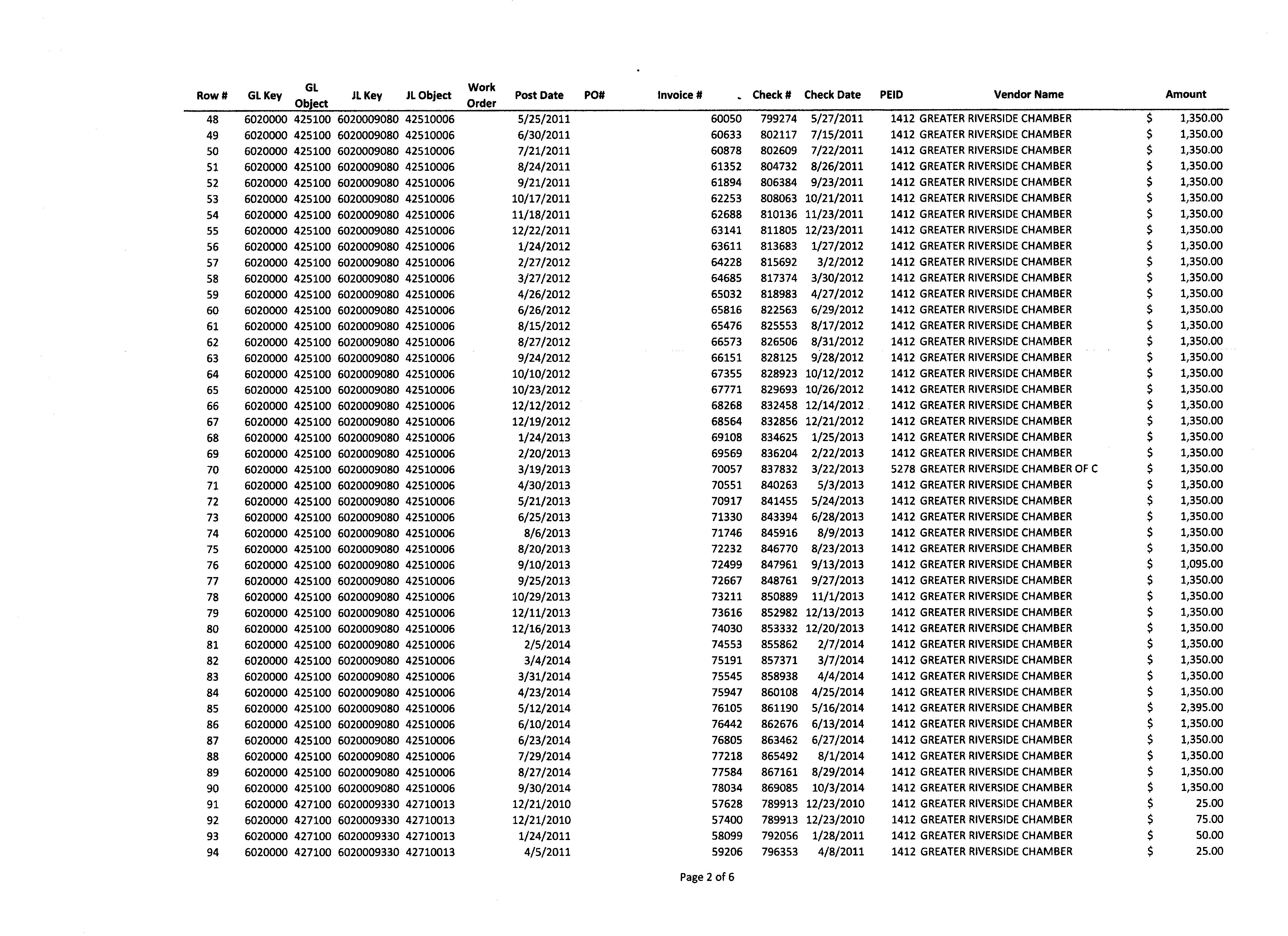

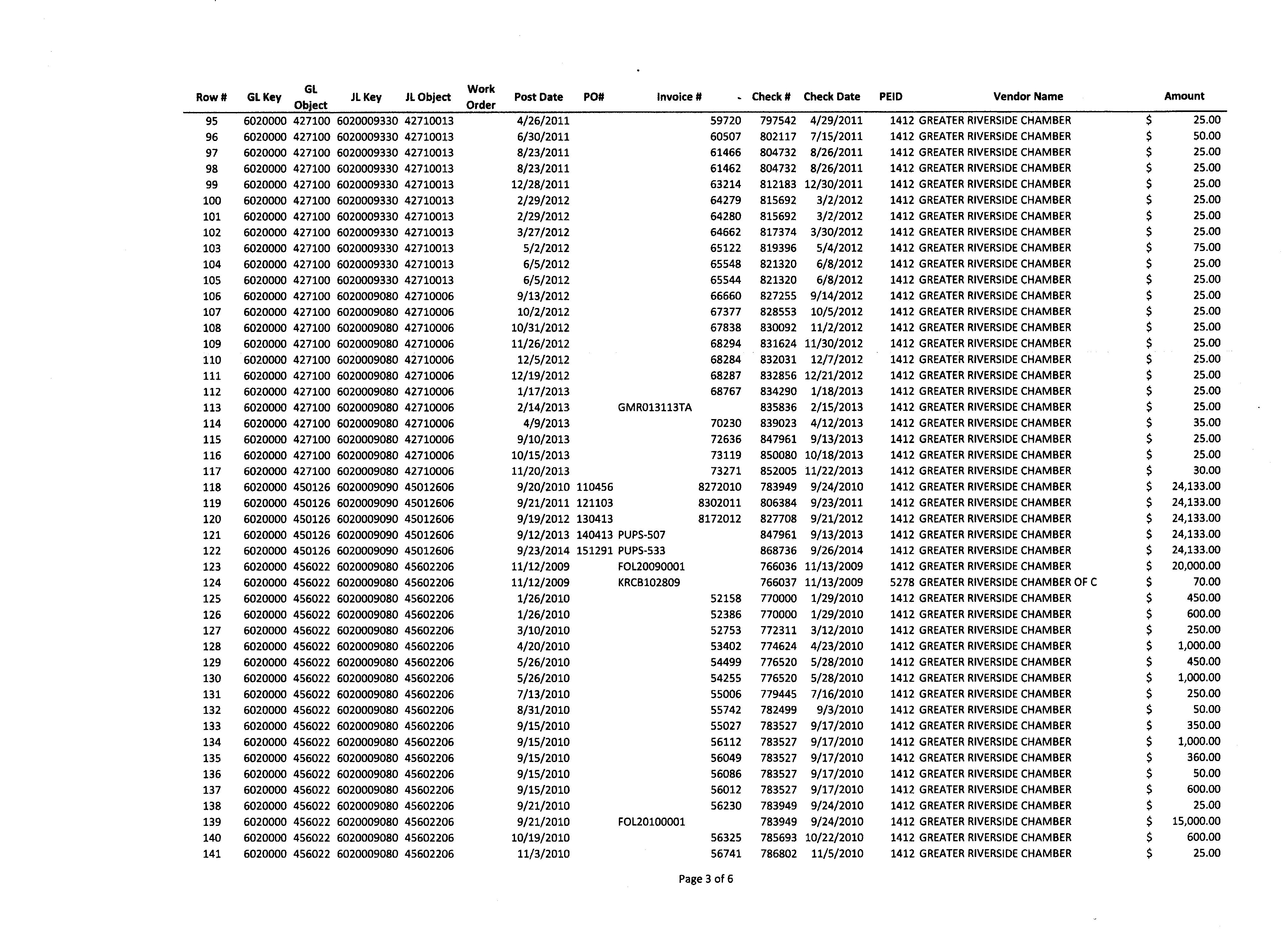

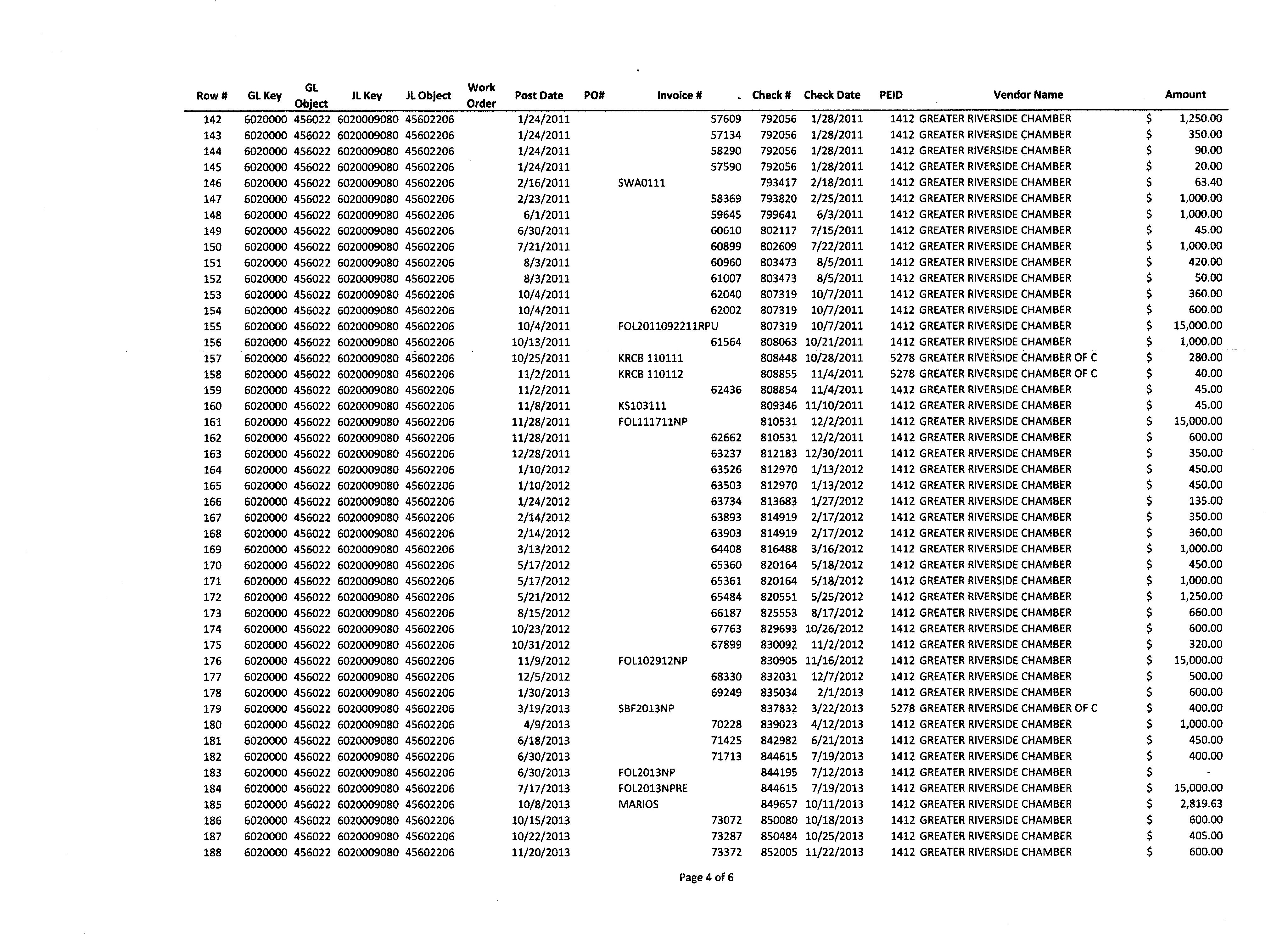

ALLEGED VIOLATIONS OF LAW COMMITTED BY THE CITY OF RIVERSIDE

1. QUESTION: Did the City of Riverside make unlawful water and electric utility revenue transfers to the city’s General Fund (GFTs) as unlawful taxes?

ANSWER: YES. Accordingly, there was never a vote of the people held to approve these special taxes as required by law. The 1955 city charter allows General Fund Transfers (GFTs) to occur up to 11.5% of the gross water and electric utility revenue each year. This GFT revenue is created by elevating the rates, fees and charges for water and electric utility services above the cost of providing the service(s). However, in the 1980s Cal. Government Code sec. 50075-77.5 (implementing language of Prop. 13) went into effect. It applies to all taxes and defines them. This Constitutional definition includes General and Special taxes. Any excess revenue above the cost of providing the publicly-owned utility service(s) is de facto a tax (either a General tax or a Special tax).

These definitions were repeated and emphasized in 1996 with the passage of proposition 218 (passed with and eighty-four percent approval).

The City of Riverside transfers this excess revenue (taxes) to the city General Fund and spends it on general government purposes. Therefore, both sources of excess Utility Department revenue are taxes subject to approval by the voters. In 1996 the voters of California approved, by an overwhelming margin (84%), Proposition 218, which added new language to the California Constitution and became effective July 1, 1997. Cal. Government Code sec. 50075-77.5 and Article 13C, sec. 2(b-d) specifically forbids the imposition, extension or increase of any Special tax without a super-majority vote on the issue of the tax. In order to lawfully collect taxes, any new or continuing rates, fees, charges and assessments above the cost of providing service had to be placed before the voters before November 8, 1998.

The City of Riverside did not hold a vote on a special tax and continued the unlawful GFTs each year for 14 years, believing it was exempt from the Cal. Govt. Code and the Constitution (Prop. 218). I can find no exemption that applies and the voters do not have the authority to void constitutional restrictions on government by voting to modify or renew the city Charter. The City did not place the issue of taxation by GFTs to a vote. Every City budget since July 1997 has included a GFT from the Water Utility Fund. This is, by its very nature, proof of the intent to collect unconstitutional water rates, fees and charges that are above the cost of providing service(s) in order to purposefully exact the GFT as an unlawful hidden tax. Article 13D, sec. 6 (b) specifically forbids the pricing of water above the cost of service and the transfer of surplus utility funds to any general government expense (See the Sacramento County Grand Jury Report dated January 6, 2010, City of Sacramento). [Please note that the City Attorney for the City of Sacramento was formerly employed in the Riverside City Attorneys’ office serving the Riverside Utility Department until December 2005.] It appears that within four years of service to the city of Sacramento her legal advice was deemed incorrect on the issues of transferring funds out of the water fund for general government purposes including paying employee salaries in other departments!

Additionally, the city of Riverside cannot transfer general government cost(s) to the water utility budget (see 2011 city budget, wherein 45 general government staff positions were transferred to the Utility Department budget). An annual budget that predicts or proposes a GFT from the Water Utility Fund without authorization from the voters is proof of intent to charge unconstitutional water rates (conclusion: intent to misappropriate funds). The California Government Code sec. 50075-77.5 and Prop 218 requires a public vote for both General and Special taxes. The Water and Electric Utility GFTs are unlawful taxes as performed by the City of Riverside. The unconstitutional water rates, fees and charges and the GFTs are documented in the city’s annual budgets and audits of the Water Utility for the last thirteen years (an audit is factual evidence of unlawful rates and GFTs). The unlawful tax established by GFTs from the Electric Utility is to be found in the annual budgets and audits as well.

This documentation establishes a pattern and practice of violating the constitution for at least the last 14 years and this process has exacted $45.million of unlawful water rates. I have not researched all the data on unlawful electric utility rates, fees and charges or GFTs for the last 13-20 years. Unlawful electrical rates exact $38 million per year of unlawful taxes (see 2009 city budget/audit). However it likely will total close to $350 million. This is an unfunded liability created by the city. Courts have ordered city general fund moneys be restored to the utility fund from which they came.

2. QUESTION: In October 2006 did the City of Riverside unlawfully approved a five-year plan of increasing water rates 50% as well as institute an unlawful, punitive 4-tier pricing scheme for water service to its customers?

ANSWER: YES. The stated intent of the scheme was to conserve water and raise water rates in order to increase the gross revenue of the Water Utility Department. This was done to effectively increase the dollar amount of the unlawful taxation by GFTs from approximately $3 million per year to over $5.5 million per year. The rate increases were stated by the city (at council meetings, budget documents and in other city documents) as being necessary to pay for the city’s “Renaissance Plan” of general government

projects.

Article 13D, sec. 6 of the California Constitution requires a public hearing before the City Council. This required hearing is held under Article 13D in order to seek a majority of written protests to the proposed new or increased water rates, fees and charges. This is required for any property-related service where the utility rates, fees and charges do not exceed the cost of providing the service and the revenue is not used for general government purposes (GFTs, Special or General Taxes). Note: electric and gas services are exempt from the requirements of Article 13D.

The City of Riverside held such a hearing (on October 6, 2006) knowing that it was acting unlawfully to approve the rate increases without a public vote. This action by the city is a clear and intentional violation of the State Constitution and the public’s constitutional right to vote on taxes (conclusion: the city exceeded its authority). Knowing that, the city continued to charge and increase unlawful water rates without seeking a public vote. These rates and the five year plan to raise them 50% was clearly above the cost of providing the service (an unlawful tax) and the city continued to benefit monetarily with ever-increasing amounts of cash revenue (unlawful GFTs) from the Water and electric Utility Fund(s) (conclusion: money is the motive that brings the city the prestige it seeks with other cities and even more so during the last three years of economic recession when we continued to spend the $1.5 billion on the renaissance plan and now more funds on “Seize your Destiny”).

The California Supreme Court published the “Bighorn Desert View Water Agency v. Verjil Cal. Supreme Court July 24, 2006, 39 Cal, 4th” decision over 2 months prior to the City Council vote to approve the rate increases that funded most of the Renaissance plan. The Bighorn decision upheld Prop. 218 and reversed the 2000 City of Los Angeles ruling. This was an earth-shaking decision for cities throughout California as it’s’ language restricts governments from raising(including borrowing money) without a vote on taxes(borrowing or incurring debt creates an automatic demand for increased city tax revenue)..

The City of Riverside therefore knew or reasonably should have known that the proposed water rates and resultant GFTs were unlawful and unconstitutional. I believe constitutional violations were intentionally planned. It was planned as a scheme to misappropriate funds as hidden unlawful taxation and unconstitutional rates, fees and charges for utility services. The city continued, regardless of the Supreme Court decision, because it needed to approve and fund its “Renaissance Plan.”

The City Charter, Article IV, gives the Mayor authority to make policy and direction of the city government actions. The Mayor instructs the City Manager, City Attorney and the City Council on policy and direction of decision making. According to the City Charter, the City Manager has “sole authority to carry out policy and direction without interference from the council members.” The City Manager reports to the Mayor.

3. QUESTION: At the time of the hearing did the city also approve dramatic increases in the electrical rates well above the cost of service?

ANSWER: YES. Article 13D does not apply to electrical fees; however, the Supreme Court wrote in the Bighorn decision that Article 13C does apply to electrical utility service provided by a (charter) city and included analysis and case law in support. All increased electrical fees that are above the cost of service are a special tax including funds transferred to the general fund! This is consistent with the meaning of Cal. Govt. Code 50075-77.5 and Article 13C requiring a vote to impose taxes. Additionally, as stated above, Riverside’s electrical rates, fees and charges are intentionally set above the cost of service. This is done to continue a reliable monthly flow of cash revenue for transfer to the City General Fund for non-utility general government expenses in-lieu of taxes denying the public its constitutional right to vote on taxes (Cal. Govt. Code sec. 50075-77.5 and Cal. Const. Article 13C).

4. QUESTION: Did the City of Riverside devise and implement a “confidence scheme” under the guise of “water conservation” in a period of “statewide drought”?

ANSWER: YES. The city planned and implemented an expanded scheme. The City of Riverside (October 2006) set water rates well above the cost of service to residential parcels and approved a punitive 4-tiered scheme to charge higher rates for those water customers who use larger than “normal or average” amounts of water (See city water rate schedules and Attachment A). To justify this unlawful, punitive tiered-rate schedule, the city basically determined that any person using more than the established “normal” amount of service must be wasting water during the “statewide drought.”

Articles in the local Press-Enterprise newspaper quote city officials as stating that there is a “statewide drought” and therefore an urgent necessity to conserve water. The city took advantage of public fears on the subject to make a finding of “Use Constituting Waste” without establishing any facts or evidence of wasteful water use or a shortage of water in the City of Riverside (See City Water Rule 15, “Water Waste”). (A state statutes say beneficial use of water for landscape irrigation is up to 21/2 acre feet per acre per year before you can begin to question its use as not beneficial and thus conclude wasteful usage of water.)

I have found no data or analysis substantiating this conclusion of “use constituting water waste” by the city. This conclusion is inconsistent with Water Rule 15 and has been and/is merely an assumption to further justify the unlawfully high rates, fees and charges necessary to carry out the scheme (see Attachment A). Additionally, the City of Riverside is not and has not been impacted by drought conditions since the mid-1960s. This occurred after a long period of tremendous local growth (post-1941 development) that created huge increases in water demand for industry, housing and public water service, all of which coincided with a cyclic period of low rainfall in the early 60’s.

You will find ample documentation of these facts in the City of Riverside’s 2005 Urban Water Management Plan, which has sections on history, supply sources, reliability of supply, charts of annual (historical and predicted future) production/use figures for water demand (in the city at full built-out population) and notes of revenue reliability and GFTs. The 2005 Urban Water Management Plan documents that, in decades going back to the founding of the city, there has not been a lasting natural shortage of water and there is no future predictable shortage until beyond year 2030. City officials have been quoted and written in city documents that “if the city needs cash we raise the (utility) rates” and “the utilities are a cash-cow even during the statewide drought of the last year”.

The Press Enterprise daily weather page reported a normal annual rainfall of 41.5 inches in the San Bernardino Mountains. Since the city’s printing of the 2005 UWMP dozens of articles have appeared in the Press Enterprise. Many times the reporter interviews and includes quotes from city officials. None of these quotes make reference to our abundant water supplies during the drought or the supporting information in the 2005 UWMP (a document prepared every five years by statute). They did not act to calm the fears of the general public to further the scheme to charge higher than cost for water service provided to each parcel in the city with monthly transfers to the general fund.

100% of our water is from huge rapidly rechargeable (from precipitation in the local mountains) ground water basins in the San Bernardino valley Bunker Hill basin and the North Riverside basin.

Because there is the potential for a too-high water table in the Bunker Hill Water Basin (the basin that provides most of Riverside’s water), in the 1980s the Court appointed a Water Master. The Water Master’s job is to annually determine how much ground water to harvest in the water basin so as to keep ground water from rising into foundations and basements in downtown San Bernardino. His primary responsibility is to maintain a depth-to-groundwater level of approximately 150 feet below the surface in order to prevent earthquake liquefaction from occurring in most of the San Bernardino Valley. Without Riverside’s annual water harvest from the San Bernardino/Bunker Hill well field, downtown San Bernardino would experience surface flooding from artesian water sources and much damage to structures would occur without the occurrence of an earthquake. There are current efforts to bring the ground water level down to 150feet and maintain it at that level to prevent recent estimates of earthquake liquefaction zones.

Riverside is not in an “emergency drought” and is not “required” to conserve a plentiful local resource we already own. The city has not declared a “Water Supply Emergency” in order to implement mandatory conservation measures because there is no drought emergency in Riverside. The state Drought Emergency Program to conserve water established a voluntary goal of 20% by 2020 and provided for communities or regions who can demonstrate their water resources are unaffected by drought limiting the supply available to them. The only exception would be in those cases where emergency shortages actually exist and mandatory conservation measures have been implemented to protect public health & safety by a local declaration of a supply/service emergency. Conclusion: the City of Riverside is using this statewide “drought scare factor” and free publicity to successfully conduct a scheme of unlawful water rates/taxation.

We the people of the City of Riverside have, over the last 98-plus years, continuously invested public funds into purchasing and improving water rights and infrastructure that currently is valued at more than one billion dollars. We continue to do this in order to benefit from a low-cost, safe, reliable and necessary water utility service that is independent of expensive imported water and therefore is also independent of drought impacts (See Water Utility “Mission Statement”). We pump local ground water, plus we own court-adjudicated rights in San Bernardino to harvest and export to Riverside more water than we can use annually.

To illustrate this more fully, one should note that the city also sells 15-18% of its annual water production to areas outside its service area. This includes the daily service of water to Home Gardens and the northern parts of Corona, as well as an additional of 6,000 to 8,000 acre feet of water to the Western Municipal Water District (2005 Urban Water Management Plan).

Conclusion: the City of Riverside is misleading the citizens of Riverside into accepting an erroneous fact of “drought” and unlawfully high water rates designed to “save” water so that, the funds “above the (much lower) cost of providing service to individual property owners/customers is sufficient to for non-water utility city expenses such as but not limited to debt service of the Renaissance and Seize your Destiny plans .

“Normal or average” water consumption in Riverside was determined by reviewing city zoning maps and property water bills to establish that the “average” customer/family lives in a residential 3-bedroom house of 1500 sq. ft. on a smaller-sized 7,000 sq. ft. lot. It should be understood that many residences in the city have a much larger lot and therefore a much larger yard to irrigate. Any tiered pricing scheme inherently charges more per measured unit of water to above-average customers than it does to average or below-average lot size customers (see Attachment A). This is in violation of Article 13D.

Conclusion: the issue of “water waste” is irrelevant to the data analyzed. It was merely a convenient conclusion to enhance this unlawful scheme so as to generate more Water Utility Department revenue for transfer to the General

Fund and to pay for planned future sale of Certificates of Participation for the Renaissance plan. The tiered pricing scheme is but a formula for calculating your usage-based rate of taxation and punishment for exceeding the city determined “normal or average customer use”. It calculates your charge for metered consumption of water service without a public vote of approval or constitutionally mandated “Due process of Law”. If you do not comply with the city’s rules you can be fined up to $1000 per violation and charged with a misdemeanor subject to jail time and fine.

The California Supreme Court Big Horn ruling reaffirmed prop 218 in total. The Court said that, in the absence of a Special Benefit determination on a parcel by parcel basis, all customers must be charged the same rate, fee or charge calculated to meet and not exceed the cost of providing service. This included but is not limited to: residential, industrial, manufacturing, agricultural, commercial, schools, hospitals, universities, colleges and any governmental entity receiving the service. In the absence of a special benefit study and voter approved assessment every customer may only be charged the same rates, fees and charges as every other customer in the city. The consumption/metered rates, fees and charges may only be established from the annual cost of electricity ($0.045 to run the pumps plus the annual cost of maintaining the infrastructure (these are the variable costs of a water utility). Fixed costs may only be attributed to the meter/availability of service charge varied by the flow capacity of your meter connection to the infrastructure in the public right of way. In spite of the emergency drought statutes that allow permission to include debt service for capital replacement, new construction or replacement of old infrastructure into the rate structure this remains a permissive act that remains constitutionally challengeable. Much of this is also the conclusion of the Sacramento Grand Jury Report, January 06, 2010.

The city has therefore unlawfully established, by ordinance, unconstitutional tiered pricing rates and 19 different water rate schedules. It also has made “special contract sales” for ongoing service with some customers for lower-cost water. The concept of having more than one price for water consumed by any customer(s) is in violation of Proposition 218 and the Supreme Court’s Big Horn ruling. The rates, fees and charges for water metered service cannot exceed the cost of providing the service to any property owner/customer and must be the same for all customers (Bighorn Desert View Water Agency v. Verjil and the Sacramento County Grand Jury Report January 2010).

Therefore it can be seen that low-priced water service for some customers of the City of Riverside has to be subsidized by water rates that are substantially higher for other customers, who are primarily the residential customers (see Attachment A). But Article 13D requires the pricing of water service by a public agency to be no more than the actual cost of service, unless a Special Benefit assessment is determined and voter approved on a parcel by parcel basis (refer to Article 13C and 13D for discussion of what constitutes a Special Benefit). Any Special Benefit assessment would be an additional charge as a property assessment on our property tax bills, and like a Special Assessment for capital improvement debt service (San Marcos Water District v. San Marcos School District, 1986). The city has not performed any Special Benefit analysis.

The City of Riverside has established and maintains a pattern and practice of violating the state Constitution. It also violates the equal application of law guaranty of both the U.S. Constitution and the State Constitution.

Conclusion: the city intentionally refuses to comply with Proposition 218 for the purpose of extracting more unlawful tax revenue from the people of Riverside than the city would otherwise receive by lawful means without seeking voter approval.

The Riverside Public Utilities Board (which consists of council-appointed volunteers) studies, decides and recommends water and electric utility rates for approval by the City Council. A Board member told me that the City Attorney and the City Manager wanted nothing but increased water and electric rates on punitive tiered-rate schedules recommended to the city council.

Before the end of 2006, the board and the city needed to complete the approval of the specified rate increases and the punitive 4-tiered schedule in order to provide the General Fund with an enhanced steady monthly cash flow to the general fund. This cash flow was needed so as to justify a high (AA++) bond rating in following years (2007-2009). A high bond rating ensures the marketability for the proposed issuance and sale of Revenue bonds and Certificates of Participation (COPs). Both of these financial instruments were intended to fund parks, libraries, roads, and railroad separation projects (general government expenses) that were part of Riverside’s “Renaissance Plan.”

It was estimated that approval of the Renaissance Plan would cost $1.5 billion over five years beginning in 2007. According to my source, she and other Utility Board members wanted to discuss other, more fair, alternatives (i.e. water budgeting per customer lot size) as other cities were doing to effect water conservation. But they were firmly directed by the City Manager’s office to only discuss and approve punitive tiered-rates and a 5-year series of annual small increases totaling 50%. This way it would impact customers in about the same manner as an annual increase in the cost of living index.

The motive is prestige and personal grandeur, in that the Mayor and other city officials are seeking to further their reputations, careers and incomes. Co-conspirators are benefiting through increased compensation via salary increases, bonuses, promotions and new employment. Examples of career enhancement are Eileen Tiechert, Steve Beck and Dave Wright, who have left the city for higher-level jobs elsewhere, or have sought to.

Conclusion: The city’s desires are to take city spending to a higher level, thereby achieving a (falsely acquired) reputation for being the “Best-Run City in California” throughout a world -wide recession.

5. QUESTION: Does the City of Riverside levy a Utility Users Tax (UUT) on the sum of the monthly billed rate charges for water and electrical service and other services including sewer, trash, phone, gas, cable TV?

ANSWER: YES. It is currently set at 6.5% and seems to have been instituted by the City Council around 2001. To my knowledge the city did not allow voters to approve this tax, which would be in keeping with its unlawful pattern and practice of avoiding any public vote on taxes. If the rates, fees and charges are unlawfully set to generate and effect unlawful taxes or GFTs (refer back to Section 1 of this paper), then, any UUT applied to the sum of the metered rate charges on each monthly bill effectively establishes “Double Taxation” another unconstitutional act.

Double taxation, as practiced by the City of Riverside, occurs when the City Utility Department includes costs of capital improvement in the billed utility consumption rate structure. The California Supreme Court in San Marcos Water District v. San Marcos School District decided that charges for recovery of capital improvement costs of a public utility are Special Assessments (i.e. taxes) and are not the cost of ongoing services. The Court also directed that these capital costs are not be hidden in the rate structure for ongoing service and established a “Bright Line Rule” and stated that form follows function in determining if a fee for services is a hidden tax. To my knowledge, the City of Riverside has always hidden the costs of capital improvement in the consumption rate of services. The city never has sought a vote of the public to approve a Special Assessment (General or Special Tax) prior to issuing municipal bonds or COPs that incur annual debt service costs to the Public Utility Department (Article 13C). Courts have also published decisions in similar cases and ruled that when government entities enter into contractual forms of debt such as municipal bonds, Certificates of Participation or any form contractual sale/lease back agreement, they create a new demand for tax revenue to pay the annual debt service throughout the contracted period (20-30 years) and thus this demand for new taxes need the voters’ approval for the city to lawfully enter into new instruments of debt. Any debt contracted by the city in the last 20+ years may be unlawful contracts.

The city consistently avoids a public vote to approve Special Assessments to pay debt service and continues to unlawfully inflate the billable amount subject to the UUT, thus effectively increasing the City General Fund revenue monthly from the UUT. This unlawfully nets the city approximately $28 million per year of UUT revenue. The UUT is unlawful because at the time of its authorization by the city Council it was levied on top of the illegal taxes hidden in the utility rates thus making the UUT the second of the two taxes that established the fact of double taxation.

Since all utility services are delivered to each person in possession of, or the owner of, every parcel in the city’s service area(s), the UUT becomes a property-related tax. The courts have determined that this form of double taxation on property is unlawful (see Flynn v. San Francisco, 18 Cal. 2d 210,215 and the cases cited therein.) Flynn v. San Francisco states: “forbidden double taxation occurs when two taxes of the same character are imposed on the same property for the same purpose, by the same taxing authority within the same jurisdiction during the same taxing period.” The City of Riverside has been charging utility customers (property owners) UUT on water and electric utility services and the hidden taxes therein, which constitutes double taxation. This is because these services are supplied directly to property owners via conduits along dedicated city easements on and under said private properties for use in the pursuit of the individuals’ right to enjoy property ownership and this effectively taxes property owners twice, in violation of Proposition 13’s one-percent limit of property taxation.

The city unlawfully implemented and maintains utility rates, fees and charges that are designed to produce unlawful tax revenues. These taxes are hidden in the utility rate structure and result in monthly surplus cash revenue transfers to the city General Fund. In effect this double taxation is intended to further increase General Fund revenue.

Conclusion: double taxation as practiced by the city is deceitful as well as unconstitutional.

6. QUESTION: Did the City of Riverside unlawfully issue municipal bonds and Certificates of Participation (COPs) since July 1997 to fund water and electric utility infrastructure improvements as well as non-utility General Fund revenue projects (See City of Riverside Capital Improvement Project(s) Report)?

ANSWER: YES. The specific individual bonds and COPs can be found at EMMA.MSRB.org. The City of Riverside has submitted incomplete or misleading information concerning the unlawfully-enhanced sources of the City of Riverside’s Utility and General Fund revenue in these matters regulated by the Securities & Exchange Commission. In addition, I believe disclosing/representing unlawful city Utility Department and General Fund revenue as lawful revenues is an attempt to fraudulently instill undeserved confidence in rating agents, investment banks and investors of the city’s ability to repay debt service (albeit with unlawful revenue).

Conclusion: misrepresenting or failing to disclose pertinent information in regulated financial instruments may be a Federal SEC violation. The city gained a monetary benefit from higher-than-deserved bond ratings and lower borrowing costs over the contractual period by placing the financial institutions underwriting the bonds at risk.

7. QUESTION: Did the City of Riverside hide capital cost(s)( mostly debt service payments) in Public Utility consumption rates, fees and charges to unlawfully increase its’ utility rates without a vote of the public as required by law?

ANSWER: Yes. “Capital Cost” is the cost of acquisition, installation, construction or reconstruction, or replacement of a permanent public improvement. Electric or Water Revenue Bonds and/or COPs are financial instruments used to borrow capital funds to finance capital improvements to the utility infrastructure. Capital costs are not operating and maintenance expenses to be included in rate calculations (Cal. Supreme, San Marcos).

Capital costs for new infrastructure are supposed to be funded with Special Assessments, Developer Fees, or new individual connection fees. COPs are contractual financial instruments of borrowing funds for capital improvement and incur the paying of annual debt service on a schedule for a finite period set forth in each contract. Again, the Supreme Court in San Marcos and other cases have determined that the debt expense (of a finite period with a stated end time) is not a cost of operating the utility service but rather is a Special Assessment or Special Tax. These require an approving vote of the public before the city can issue the financial instrument for rating and sale.

Once again, the City of Riverside has acted as if it is exempt from the constitution and law in matters of maintaining and increasing General Fund revenue. Clearly it is not–and thus the matter requires further investigation. The City of Riverside has consistently established a pattern and practice of unlawfully assigning utility debt service to the electric and water utility cost-of-service accounting ledger. These revenue-enhancing mechanisms create ever-increasing utility rates, the purpose of which is to unlawfully inflate the Utility Department’s gross revenue. These acts result in ever-larger GFTs and UUTs that are in turn used as the primary means of increasing General Fund revenue. This could be described as acts of extortion from the public and consists of multiple acts of unlawful taxation under color of authority.

It should be noted that there is a difference between fixed costs and variable costs. Debt service expenses are fixed costs of providing the service and are not to be included in the variable costs that figure into rate calculations. Fixed costs of a contractual nature (bonds and COPs) are the result of public capital improvement project planning and constitute taxation to pay the debt service. The fixed cost of debt service is defined in law as a Special Assessment. Special Assessments must be voted upon and must be listed separately on the billings; by that means, the customers can see each item of debt service and its ending date as it is paid down. In that way, the total debt service is not on the bill and so is never subject to the UUT.

Conclusion: the City of Riverside hides utility debt service in rate calculations for both electric and water service. This is purposely done so the public consumer will not see it as a tax issue or understand that he/she has a constitutional right to vote on the subject new taxes(Articles 13A, 13B and 13C). Also, the public will never see the end of the debt obligation in the billings, since the city’s scheme is to never decrease these ever-so-profitable rates, fees and charges even when the debt is paid off or retired. (Refer to: Article 13C, definition of General tax, Special tax, capital cost, cost of service; Cal. Govt. Code sec. 50075-77.5, definitions and voter requirements for General and Special taxes; and San Marcos.)

8. QUESTION: Is the City of Riverside disguising the true nature of COPs to protect its scheme?

ANSWER: YES. COPs are contractual lease-back agreements of borrowing in a regulated financial market. The documentation in the COPs clearly states they were created to avoid constitutional restrictions or limits on the amount of debt a municipality can enter into. They are created to avoid the provisions of law that require a vote before issuance. They are not included or counted in the state-mandated 15% of total property valuation that limits local government borrowing (Article 13B). The city will borrow as much as the markets will loan on these instruments. It has not disclosed this to the public, in spite of the public testimony of many citizens who have spoken at council meetings over the years. This testimony was on the specific subject of the 15% limit on borrowing–as well as the seemingly large amounts of debt the city has undertaken (approximately one billion dollars since 2006).

Conclusion: again, the city’s evasive deceitful nature is shown by its pattern of not responding to its citizen’s questions accurately and honestly. This constitutes more evidence of the how the City of Riverside unlawfully protects what it perceives as its own interests and placing the citizens of the city at risk of future debt payments we cannot afford or file for bankruptcy without exercising their constitutional RIGHT TO VOTE.

9. QUESTION: The above unlawful actions of the City of Riverside generate approximately $70 million per year of General Fund revenue made in 12 monthly payments of the budget cycle. The City has obligated much of this unlawful revenue to contractual obligations to pay for almost $1 Billion dollars of borrowed funds. Did the City of Riverside intend to maintain this scheme should a legal challenge to it come forward?

ANSWER: YES. The U.S. Constitution has a “contract impairment clause” that, if invoked, should prevent a legal challenge from terminating the unlawful sources of revenue that have been pledged to pay the city’s contractual debt obligations. Undoubtedly, the city will use this clause in its defense. I believe you will find that the facts are evidence of the intent to create a scheme that will be virtually impossible for the citizens of Riverside to terminate. The showing of fact that the city intentionally entered into a contract using unlawfully obtained funds is in itself unlawful and nullifies these contracts. The U.S. constitutions contract limitation clause is not intended to allow illegal acts established to further a contractual instrument of debt to be created or maintained. We must protest and proclaim that the all of the utility contractual debt service must be paid only with lawful General Fund revenues (as part of restitution to the ratepayers). Doing so will eliminate from utility budget/rate calculations all of the debt service expense that has unlawfully been imposed upon the consumer public. This is the answer to all who complained about $1000-3000 summer electric bills at city Council meetings in 2008-9

Conclusion: Directing that the city’s General Fund pay the Utility Department’s debt expense with lawful revenues only will help compensate the public for damages and is in fact pledged by the city in the COPs document(s) as the form of backup payment in case the law is enforced upon the city.

10. QUESTION: In 2006 the Riverside County Grand Jury issued its report on the ineffective efforts of the City of Riverside and the North West Mosquito Vector Control District (District) to protect the general public health from transmission of the West Nile Virus (WNV). The Grand Jury reported seven WNV cases in the City of Riverside and directed the city to perform better. The City Manager responded, saying the city’s efforts were appropriate and too costly to improve. Did the City of Riverside create a scheme with the District by proposing to annex it into the District and propose an unlawful Special Assessment on residential properties within the city ($8 per acre/lot)?

ANSWER: YES. A Special Assessment is unlawful because of the San Marcos ruling that Special Assessments are only to be used for capital improvement costs including debt service expense for capital construction. The engineering detailing how this would correctly be an annual property assessment erred in listing only $16,000 of a $488,000 budgeted for services. The District Board approved resolutions Nos. 460 and 462. These almost identical resolutions make the agreement to annex the city into the District and make a $0.00 transfer to the District of ad valorum property tax revenues generated within the territory to be annexed (tax revenue presently passed to the City of Riverside by the County Assessor). These tax monies were intended to remain in the general fund for other city spending opportunities ($488,000 per year). So both parties stood to gain essentially $488,000 and you would see a new annual property tax on your bill! Such a deal!

The San Marcos Supreme Court ruling stated that Special Assessments are only to be used to recover capital costs of a permanent improvement (i.e., actual constructed infrastructure) and not a fee in lieu of taxes. “A fee constitutes a Special Assessment only if its purpose is to defray the costs of capital improvements that directly benefit the property.” The San Marcos decision says utility services are property-related services; yet, under state law mosquito/vector control is a 100% public health program (that benefits the general public). All of the Districts’ public literature emphasizes the general public benefit of this public health based program to control or eliminate mosquitos, rats and Africanized bees.

This state-mandated program continues today as the “The Mosquito Abatement and Vector Control District Law” (Health and Safety Code Sec. 2000-2007) and the District is eligible to receive annual state funding from the Vectorborne Disease Account (H&S Code, Section 116112). The District is also supported with an appropriate share of ad valorum property taxes (from properties in the district). San Marcos “established a rule that looks to the purpose of the fee being charged, and not simply to the form of the fee, a matter which can easily be manipulated.” Therefore, in this case the City of Riverside and the District are unlawfully manipulating the situation and the supporting documentation to annex territory to the District and establish a never-ending, unlawful Special Assessment on property ownership. Also, they never intended to assess any of the city owned property or commercial/industrial properties. The city placed this extra cost in your proposed property assessment. Such a deal!

So here is the motive behind what the city and the District are doing: San Marcos also determined that local government (the city) is exempt from Special Assessments on city-owned property. Thus all the city’s costs are assigned to and paid by the private property owners through the proposed unlawful Special Assessment regardless of where the diseases and vectors are found. Conveniently, by law the city is exempt for all costs to treat city-owned parks, golf courses or any other habitat for any vector on any city property—when the District uses a Special Assessment to recover the costs of service.

It seems apparent that the District agreed to this scheme to let the city keep the ad valorum property taxes as part of this sweet deal. The new assessment will generate over $488,000 for the District with annual inflation cost increases of 2-3%. Did the City of Riverside pay the cost of this annexation? In San Marcos the “court concluded that to focus exclusively on whether the charge at issue is in the form of a Special Assessment or user fee would elevate form over substance and permit local government to evade the prohibition on charging public entities.” The situation here is that the city and the District are merely trying to reverse the logic of the above quote, i.e., that the city and the District are using “form over function” to disguise and evade the true meaning and lawful application of “Special Assessment.” Special assessment is now charged to government owned property receiving public utility services.

The city and District alleged the annual program costs are “improvements to property.” This was conceived so both entities will benefit from revenue enhancement at the expense of property owners in the city. The Court in San Marcos ruled that capital costs are for permanent improvement to property (example: utility infrastructure) and are only recoverable through a Special Assessment. Annual operating expenses for a public health program to control disease vectors is not a capital expense and thus as proposed is an unlawful Special Assessment. The votes were not counted at the public hearing to determine the tally as required by constitutional law. Instead several passed before the Press Enterprise published a small article on the voters disapproval of the ballot measure. The article did not say how many yes or no votes were counted!? The city of art and innovation.

Ad valorum property tax revenue from the city general fund and/or a new Special tax are lawful forms of paying the District’s cost of providing this service to the citizens of Riverside. The city has yet to announce a contract with the NWMVCD to pay the cost of service from the general fund. Such a Deal. Appropriate taxation must be vote on in this case to pay the cost of ongoing variable expenses for a general public health benefit (for vector control services). The City of Riverside cannot claim an exemption from a Special tax.

Conclusion: the District should be putting to a vote both the annexation and a Special Tax (H&S Code Sec. 2081). Otherwise, this is just another form of conspiracy against taxpayers by the city and District. Excessive greed is evidenced by their actions.

11. QUESTION: Did the City of Riverside establish a lawfully binding contract with the utility rate-paying citizens of Riverside when it established and published in numerous city documents through many years the following Mission Statement?

“The City of Riverside Public Utilities Department is committed to the highest quality water and electric services at the lowest possible rates to benefit the community.”

ANSWER: YES. I believe that under common contract law, the City of Riverside did establish an actual lawful binding contract with the people of Riverside when it adopted and published, openly, the above mission statement. In fact, a written contract is also established when you apply for utility services from the city Public Utility Department. I believe the second includes the former. Both being provisions of the binding agreement.

Conclusion: the City of Riverside violated the lawful contract with its citizens and utility customers when it established public utility rates above the cost of service, which is a violation of the Constitution of the State of California.

12. QUESTION: Should the reader find facts and truth in the above?

ANSWER: YES. The reader should easily find that: elected and/or employed individuals in the City of Riverside have, on numerous occasions, violated (with intent) the laws and constitutional protections and rights of the citizens of Riverside. These violations include, but are not limited to, the right of the citizens to vote on taxes; thus, the City of Riverside and individuals did violate the law and both federal and state constitutions. They also thereby violated their Oaths of Office and may be punishable under federal and state laws. [Cal. Const. Article 20, sec.3; U.S. Code 42, Chapter 21, Sub Chapter 1, sec. 1981; Public Law 96-303 (1980), section: I-X]

- The reader should read the U.S. Attorneys Handbook on successful prosecution of mail/wire fraud. Mail fraud is the creation of a scheme to separate a person from something of value and uses the mail/wire to further the scheme.

The City mails you your utility bill and public notices of rate increases. You may mail your payment or use the internet for electronic payment.

Attachment A

City Development Department staff and the City Manager determined that the average Riverside utility customer occupies a single-family home on a 7,000 sq. ft lot that is zoned R-1. Many R-1-zoned single family residences are built upon lots larger than 7,000 sq. ft. Corner lots are always larger than others along a residential street and some developments in Riverside have lot sizes ranging up to several acres. But City Code Chapter 16 requires all property owners to landscape, maintain and irrigate all portions of a lot that face a public street.

All lots are subject to this code requirement, and the water rates were developed for the average 7,000 sq. ft. lot, which have about 1500 sq. ft. front yards. But many lots have much more of their square footage facing the public streets, and so do not fit the “average” criteria. Owners of large lots and corner lots are required by City Code Enforcement ordinances, and under threat of fines and penalties, to water and maintain much larger square footages of landscaping (in my case, this is an area of more than 30,000 sq. ft.). This automatically forces me into the upper tiers of water pricing, with no consideration made for my individual circumstances. In 1997, my monthly water rate was $0.47/ccf. Under the current 4-tiered system, my average monthly water rate is $3.00/ccf. Summer water bills that used to be $75 a month rose to over $600 a month. By installing city-approved water-conserving sprinkler heads and not watering portions of our large front yard (and potentially incurring fines from the city), we have reduced this amount to about $500 per month in the summer months.

The alternative, as encouraged by the city, is to put in drought-tolerant landscaping and drip irrigation, which while commendable, is a very expensive proposal for large-frontage properties. And this is all because the city wants more money in its General Fund and is collecting it in an unlawful manner in a city which admits the fact that its water supply is not affected by drought.

Additionally, most developed residential lots have one or more city trees planted in the public right-of-way along the sidewalk. City Code requires property owners to adequately water the city-owned trees. Both requirements further the city’s fraudulent revenue enhancement scheme of ever-increasing utility rates and the Utility Users Tax.

The calculations below demonstrate the disproportionate and unlawful affect of the City of Riverside’s punitive 4-tiered pricing schedules for water and electricity. Tiered pricing schemes are unlawful under Prop 218 because they exceed the proportionality rule/test and effectively charge one customer a different rate than another customer. The Supreme court upheld Prop 218 and ruled rates charged to all customers must be the same, not exceed the cost of service to the parcel, and can only be different based upon a special benefit determination on a parcel by parcel basis.

AVERAGE WATER USER:

0-15 ccf metered consumption @ $1.04 per ccf 15 ccf=$15.60

16-35 ccf metered consumption @ $1.71 per ccf 20 ccf=$34.20

36-60 ccf metered consumption @ $2.59 per ccf 10 ccf=$25.90

Totals 45 ccf $75.70

Result: Monthly cost per ccf: $1.68

BELOW-AVERAGE WATER USER:

0-15 ccf metered consumption @ $1.04 per ccf 15 ccf=$15.60

Totals 45 ccf $75.70

Result: Monthly cost per ccf: $1.04

ABOVE-AVERAGE WATER USER:

0-15 ccf metered consumption @ $1.04 per ccf 15 ccf=$15.60

16-35 ccf metered consumption @ $1.71 per ccf 20 ccf=$34.20

36-60 ccf metered consumption @ $2.59 per ccf 25 ccf=$64.75

61-160 ccf metered consumption @ $3.66 per ccf 100 ccf=$366.00

Totals 160 ccf $480.55

Result: Monthly cost per ccf: $3.00

Conclusion: The more you use, the more you pay per unit of water or other utility services (electricity) that are metered and priced on a punitive tiered scheme violating the provisions of Prop 218.

A possible investigative job for the DA? Maybe when he’s not busy..

THE PURPLE PIPE

Many have not heard of the purple pipe or if they did, do not know what it is all about. The City would like to install the purple pipe in your homes and businesses in order to reclaim the water that goes down your drain. Why ‘purple’? This is to distinguish and make sure pipes are not crossed between potable (water suitable for drinking) and non-potable (water not suitable for drinking, which will be the purple pipe. Purple pipe is for non-potable gray-water. Gray- water is wastewater from shower drains, bathtubs, sinks, dishwashers and washing machines. This gray water accounts for between 50-80% of our home, offices, and schools outflow. Gray water can be reused for irrigation, toilet flushing and exterior washing.

But we also have to remember that the City of Riverside owns water right unlike other cities. In their defense of water reclamation they also state a portion will be used to recharge local ground water levels. It is known that we use approximately 40% of our water, the remaining 60% is sold to other municipalities. In some areas of our water harvesting basin, the ground water levels cannot rise above the 50 foot mark from the ground, otherwise the risk of damaging building an infrastructure would be high. For a 5/8″ to 3/4″ pipe the rate will be $2.00 for 2012, but in 2012 it will go up to $4.00. Also what is being voting on, and the language is vague, is rate range from $3.34 to $333.34, and this without a vote of the people.

RATES 2012 RATES 2013

Therefore, we are attempting to clarify the language of the following in regards to rate cost to residents:

(1) A monthly recycled water charge based on meter size to all water rates of approximately $2.00 for residential and non-residential customers with meter sizes from 5/8” to 3/4”, effective May 1, 2012 (except for WA-2, WA-5, WA-8, and WA-10 rates). A monthly recycled water charge for other meters, ranging from $3.34 to $333.34, will be levied and will be dependent on the size of the meter.

(2) An increase to the monthly recycled water charge based on meter size to all water rates of approximately $2.00 for residential and non-residential customers with meter sizes from 5/8” to 3/4”, effective May 1, 2013 (except for WA-2, WA-5, WA-8 and WA-10 rates). An increase to the recycled water monthly charge for other meters, ranging from $3.34 to $333.34, will be levied and will be dependent on the size of the meter.

The language is vague, but it indicates a flat monthly charge depending on pipe size, then an additional increase in monthly recycled water charge which we need to clarify with the city. Further there is no difference in price between clean water and recycled water, they both will cost the consumer $1.14 per 100 cubic feet. You would expect a price break on reclaimed water. Many our asking if this a scheme or artifice? In less technical terms, a scam against the citizens of Riverside? Since the City of Riverside has water rights and doesn’t have to purchase water from a third party as many other cities do.

One thing for sure is that the rates will increase a 100% from 2012 to 2013. Many questions will continue to abound for a city that has more water than it knows what to do with it. Get more information on the purple pipe program works can be followed by clicking this link. Or the City of Riverside link: http://www.riversideca.gov/utilities/admin-publichearing.asp Will the purple eat away at constituents in taxes, and then be known as ‘The Purple People Eater”?

TMC, RATED RIVERSIDE’S MOST “SLANDEROUS” AND MEZZSPELLED, “MISSPELLED” AND “OPINIONATED” BLOG SITE! TEMPORARILY BLOCKED BY THE CITY OF RIVERSIDE AT PUBLIC ACCESS SITES WITHIN THE CITY, THEN UNBLOCKED. I GUESS YOU CANNOT DO THAT ACCORDING TO ACLU. RATED ONE TWO STAR OUT OF FIVE IN TERMS OF COMMUNITY APPROVAL RATINGS.. TMC IS NOW EXCLUSIVELY ON FILE WITH THE COUNTY OF RIVERSIDE’S DISTRICT ATTORNEY’S OFFICE, AND PROSSIBLY POSSIBLY ON FILE WITH THE CITY OF RIVERSIDE’S POTENTIAL SLAPP SUIT LIST… WE WILL HAVE TO ASK GREGORY ABOUT THAT ONE… AGAIN, THANK-YOU COMMUNITY OF RIVERSIDE AND THE CITY OF RIVERSIDE EMPLOYEE’S FOR YOUR SUPPORT! COMMENTS ALWAYS WELCOMED, ESPECIALLY SPELL CHECKERS! EMAIL ANONYMOUSLY WITH YOUR DIRT OR FOR CONTACT! THIRTYMILESCORRUPTION@HOTMAIL.COM